Savings Rate vs Investment Returns: What Matters More Depends on Your Portfolio Size

Savings rate or investment returns: which matters more? It depends on your contribution-to-portfolio ratio. The math, the five-stage lifecycle, and a calculator that names your current bottleneck.

Personal finance has a long-running argument: does your savings rate matter more than your investment returns, or the other way around? The answer depends on one number you can compute in seconds, and that number changes across your life. Early on, how much you invest dominates. Later, how your portfolio is invested dominates. The skill is knowing when the baton passes from one to the other.

The short version

Savings rate matters most when your contributions are large relative to your portfolio. Returns and asset allocation matter most when your portfolio is large relative to your contributions. The diagnostic is the contribution-to-portfolio ratio: your annual amount invested divided by your portfolio size. Watch it fall as you age, and you can see the moment your attention should shift from saving to allocating.

The math: one ratio tells you which lever to pull

In a single year, a portfolio changes by roughly what you add plus what it earns:

where is the portfolio, is the annual amount invested, and is the return. The contribution-to-portfolio ratio compares the two forces:

A high ratio means new saving moves your wealth more than the market does, so the savings rate is your lever. A low ratio means a normal market move dwarfs a year of saving, so allocation and risk are your levers. The two forces are equal when:

Invest $20,000 a year and expect a 5% real return, and your expected annual return equals your annual contribution once the portfolio reaches about $400,000. Below that, contributions are the larger annual force. Above it, returns increasingly drive the dollar outcome. The same ratio works at every stage:

| Investor | Portfolio | Annual invested | C/W ratio | What matters most now |

|---|---|---|---|---|

| New investor | $25,000 | $20,000 | 80% | Savings rate and income |

| Mid-career saver | $500,000 | $30,000 | 6% | Savings and returns both |

| Near-retiree | $2,000,000 | $30,000 | 1.5% | Returns, allocation, risk |

| Retiree | $2,000,000 | −$80,000 | −4% | Withdrawal rate and sequence risk |

Returns still matter: early dollars compound for decades

A common shortcut compares one year of contributions to one year of returns and concludes that returns barely matter for young investors. That understates returns, because a young investor’s early dollars compound for decades. Start from zero and invest $20,000 a year at a 5% real return:

| Horizon | Ending wealth at 5% | Earning 6% instead of 5% | Saving $25k instead of $20k |

|---|---|---|---|

| 5 years | ~$111k | +~$2k | +~$28k |

| 10 years | ~$252k | +~$12k | +~$63k |

| 20 years | ~$661k | +~$74k | +~$165k |

| 35 years | ~$1.81M | +~$422k | +~$452k |

| 40 years | ~$2.42M | +~$679k | +~$604k |

Illustrative, starting from $0 at a 5% real return. Over a full career, a one-point return difference and a $5,000-a-year saving difference end up in the same ballpark, because both early saving and early returns compound for decades.

Early in the journey, the savings rate sets the size of the snowball. Later, asset allocation controls how the snowball rolls. Nick Maggiulli’s “just keep buying” work makes the same point on a time axis, with a crossover year when returns first outrun contributions; our guide to that rule has a calculator for your own crossover year. This guide takes the snapshot view: at your current portfolio size, which lever dominates today?

What is your bottleneck right now?

Compare a year of contributions to a year of expected returns. When contributions dominate, your savings rate is the lever. When returns dominate, allocation and risk take over. The crossover sits at a portfolio of roughly your annual contribution divided by your return.

Investable assets you already hold.

What you add each year. Set negative to model retirement withdrawals.

After inflation. 5% is a common long-run planning number.

Contribution-to-portfolio

6.7%

Balanced.

This year

$20k in

vs $15k expected return on the portfolio.

Returns overtake at

$400k

Portfolio where a year’s expected return equals your contribution.

Drawdown shock

3.0 yr

A 20% drop equals this many years of contributions.

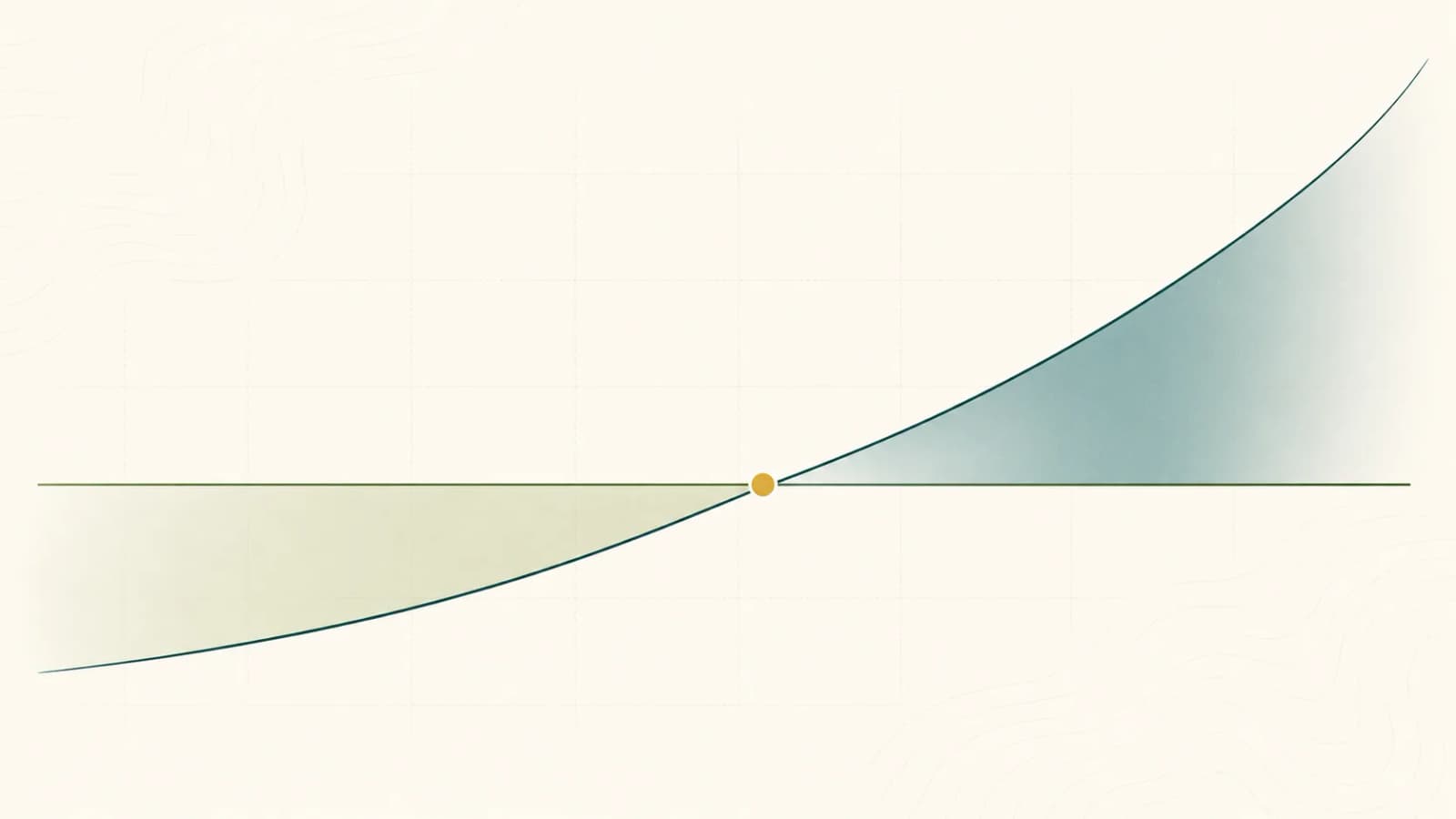

A year of contributions vs expected return, by portfolio size

Left of the crossing, your contributions move the portfolio more than returns do. Right of it, returns dominate.

Educational diagnostic, not advice or a forecast. It compares one year of cash flow to one year of expected return to show which lever dominates now; expected return is your assumption, and the tool ignores taxes, volatility, and sequence-of-returns risk.

How the bottleneck changes over the lifecycle

1. Starting out or negative net worth

The biggest levers are income, paying off high-interest debt, building an emergency fund, capturing the employer match, and automating contributions. The portfolio is tiny, so a 10% market move on $5,000 is $500, while a $500 monthly habit is $6,000 a year. Getting money invested at all dominates the spreadsheet. Allocation still matters enough to avoid real mistakes: sitting in cash for years, buying high-fee products, or panic-selling a downturn. For 2026 the IRS sets the 401(k) employee deferral limit at $24,500 and the IRA limit at $7,500.6

2. Early-career accumulation

Savings rate, income growth, lifestyle-creep control, low-cost broad diversification, and filling tax-advantaged space are the levers. A young investor can spend endless energy comparing funds when the bigger move is raising annual invested dollars. The practical plan is to choose one sensible low-cost diversified portfolio, automate it, and put most of your attention on earning and saving more. See Grow Income Faster Than Expenses and High Income Is Not Wealth.

3. Mid-career accumulation

This is the transition zone. Someone with $500,000 investing $30,000 a year sits at a 6% C/W ratio, right in the range of a reasonable long-term real equity return. The portfolio is no longer a rounding error. A bear market can erase several years of contributions, though contributions can still buy meaningfully into the downturn. Taxes, asset location, rebalancing, concentrated employer stock, and housing decisions start to carry real dollars.

4. Late career and pre-retirement

At $1.5M to $3M, annual contributions may be only 1% to 3% of the portfolio, and a normal market year can move it by more than a full year of salary. Allocation, sequence-of-returns risk, tax planning, spending flexibility, and retirement-date flexibility take over, because the portfolio now has to fund a liability: future spending. See sequence-of-returns risk and lifecycle asset allocation for the allocation math.

5. Retirement and decumulation

The sign flips. Instead of adding, you withdraw, and the relevant ratio becomes the withdrawal rate:

A retiree drawing 4% is exposed to sequence risk: weak returns early in retirement can permanently impair the portfolio because withdrawals continue while assets are down. Bengen’s historical withdrawal-rate research is built around exactly this decumulation problem.8 Our safe withdrawal rate guide covers the strategies.

What the research says

Modern lifecycle investing treats portfolio choice as a lifetime decision, not a one-time pick. Samuelson’s and Merton’s 1969 work on lifetime portfolio selection set that framing.12 The lifecycle literature adds a large asset that never appears on a brokerage statement: human capital, the present value of future earnings. Cocco, Gomes, and Maenhout find that because labor income substitutes for riskless assets, the optimal equity share is roughly decreasing over life; Viceira similarly finds employed investors can hold more stock than retirees, with labor-income risk reducing that share.34 Empirically, Fagereng, Gottlieb, and Guiso, using Norwegian tax-registry data, document a two-part adjustment: households rebalance toward safety approaching retirement, then many exit stocks after retiring.5

Long-run data supports owning risky assets for long horizons, as compensation for risk rather than a guarantee. The UBS Global Investment Returns Yearbook 2026 (Dimson, Marsh, and Staunton) reports that U.S. equities compounded at about 6.6% real per year from 1900 to 2025, against 1.6% for bonds and 0.5% for bills, across a database of 35 markets (21 with continuous histories since 1900).7 That equity premium is why an accumulation portfolio leans toward stocks, and why the dollar impact of allocation grows as the portfolio grows.

Behavior decides whether contributions actually happen. Madrian and Shea showed automatic enrollment sharply raised 401(k) participation, and Choi, Laibson, Madrian, and Metrick summarized the “path of least resistance”: plan design and defaults shape saving and allocation more than intentions do.910 For a DIY investor, automating the contribution usually beats motivating it.

Why this matters for DIY investors

Match your attention to your actual bottleneck. For a young investor, the binding constraint is rarely fine-tuning expected returns; it is getting enough dollars into a diversified portfolio consistently. For a high earner, it is often lifestyle inflation, tax-advantaged account use, concentrated employer equity, and whether income growth is becoming assets. For an older investor, it is avoiding a portfolio mistake that overwhelms decades of good saving. The ratio keeps you from two opposite errors: young investors over-optimizing allocation while under-saving, and older investors leaning on “save more” after the portfolio is already large enough that allocation and risk dominate.

Fees are a lifecycle issue too. The SEC notes that fees reduce the amount left to compound, and small-looking fees add up: on a $100,000 portfolio growing 4% a year for 20 years, a 1.00% annual fee instead of 0.25% costs about $29,000.11 Fees compound for decades when you are young, and they apply to a larger base when you are old.

Who this is for, and who it is not

This framework helps most for:

- Early-career investors choosing where to put their energy.

- High earners with strong income but weak conversion into assets.

- DIY investors juggling 401(k), IRA, HSA, Roth, and taxable accounts.

- FIRE and coast-FIRE readers who already think in savings rate and portfolio size.

- Mid-career investors deciding when allocation deserves more attention.

It is less complete for:

- People with unstable income or high-interest debt, where liquidity and payoff come first.

- Near-retirees with pensions, annuities, rental income, or business equity, where the portfolio is only part of the balance sheet.

- People with concentrated startup equity, employer stock, or real-estate-heavy net worth.

- Very low-income households, where “save more” needs the context of wages, benefits, debt, childcare, and housing.

Frequently asked questions

Does savings rate matter more than investment returns?

It depends on your contribution-to-portfolio ratio. When your annual contribution is large relative to your portfolio, saving more moves your wealth more than returns do. Once the portfolio is large, a year of returns dwarfs a year of saving, and allocation and risk matter more.

When do investment returns start to matter more?

Around the point where your portfolio reaches your annual contribution divided by your expected return. At $20,000 a year and a 5% real return, that is about $400,000. Past there, expected returns add more dollars in a typical year than your contributions do.

What is the contribution-to-portfolio ratio?

It is your annual amount invested divided by your current portfolio value. A high ratio means you are in the savings-driven phase; a low ratio means you are in the returns-driven phase. It falls naturally as your portfolio grows.

Should young investors ignore asset allocation?

No. Pick one sensible, low-cost, diversified portfolio and automate it, then put most of your energy into saving more. Allocation still matters enough to avoid large mistakes like sitting in cash, paying high fees, or selling in a panic.

How does this flip in retirement?

You stop adding and start withdrawing, so the relevant number becomes your withdrawal rate, spending divided by portfolio. At that stage, sequence of returns and a sustainable withdrawal rate dominate the outcome.

Key takeaways

- Compute the contribution-to-portfolio ratio. Annual invested dollars divided by portfolio size tells you whether saving or returns matters more right now.

- The crossover is near W ≈ C/r. Below it, contributions dominate; above it, returns dominate.

- The bottleneck moves over the lifecycle. Saving early, allocation and risk in the middle and late stages, withdrawal rate and sequence risk in retirement.

- Returns still matter for the young. Early dollars compound for decades, so a low-cost diversified portfolio plus a high savings rate is the combination that builds wealth.

- Match your attention to your bottleneck. Saving when the ratio is high, risk management when it is low.

Related guides

- Just Keep Buying covers the crossover on a time axis, with a calculator for the year returns first outrun your contributions.

- Lifecycle Asset Allocation covers the allocation question, how human capital sets your stock share and glide path.

- Grow Income Faster Than Expenses covers the savings side when the ratio is high.

- Sequence-of-Returns Risk covers the pre-retirement and decumulation danger.

- Safe Withdrawal Rate covers the decumulation phase where the ratio goes negative.

- High Income Is Not Wealth covers turning a high income into the portfolio that eventually dominates.

Sources

- Samuelson, P.A. (1969). Lifetime Portfolio Selection by Dynamic Stochastic Programming. Review of Economics and Statistics, 51(3), 239-246.

- Merton, R.C. (1969). Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case. Review of Economics and Statistics, 51(3), 247-257.

- Cocco, J.F., Gomes, F.J., & Maenhout, P.J. (2005). Consumption and Portfolio Choice over the Life Cycle. Review of Financial Studies, 18(2), 491-533. The optimal equity share is roughly decreasing over life.

- Viceira, L.M. (2001). Optimal Portfolio Choice for Long-Horizon Investors with Nontradable Labor Income. Journal of Finance, 56(2), 433-470.

- Fagereng, A., Gottlieb, C., & Guiso, L. (2017). Asset Market Participation and Portfolio Choice over the Life-Cycle. Journal of Finance, 72(2), 705-750. Households rebalance toward safety before retirement and exit stocks after.

- Internal Revenue Service. 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500.

- Dimson, E., Marsh, P., & Staunton, M. (2026). UBS Global Investment Returns Yearbook 2026. U.S. 1900-2025 real returns: equities ~6.6%, bonds ~1.6%, bills ~0.5% per year; 35 markets, 21 with continuous histories since 1900.

- Bengen, W.P. (1994). Determining Withdrawal Rates Using Historical Data. Journal of Financial Planning, 7(4), 171-180.

- Madrian, B.C., & Shea, D.F. (2001). The Power of Suggestion: Inertia in 401(k) Participation and Savings Behavior. Quarterly Journal of Economics, 116(4), 1149-1187.

- Choi, J.J., Laibson, D., Madrian, B.C., & Metrick, A. (2004). Saving for Retirement on the Path of Least Resistance. Defaults and plan design shape saving and allocation.

- U.S. Securities and Exchange Commission (Investor.gov). How Fees and Expenses Affect Your Investment Portfolio. A 1.00% vs 0.25% fee costs about $29,000 on $100,000 over 20 years at 4%.

More in Investing & Portfolio

Browse all investing & portfolio guidesGet new guides by email

Evidence-based, no jargon. At most two emails a month. Unsubscribe any time.

Try it in Summitward

See FI progress tracking in action with your own financial data. Free to start, no credit card required.