Portfolio Risk Is More Than Volatility: Drawdowns, Pain Index, and Ulcer Index for DIY Investors

Volatility describes how returns vary. Pain describes how it feels to live through them. Learn when each risk metric matters: standard deviation, max drawdown, time underwater, Pain Index, and Ulcer Index, with a side-by-side calculator using 98 years of Damodaran return data.

What "Risk" Actually Means

Ask three investors what risk means and you will get three different answers. One says volatility, the day-to-day swings. Another says permanent capital loss, money that does not come back. A third says the chance of failing to meet a goal: not having enough at retirement, or running out in old age. Behavioral economists add a fourth: the risk of selling at the wrong time because the path was too painful to hold.

All four are real. The mistake is picking one and ignoring the others. Standard deviation does not capture what a 60-month bear market feels like. Maximum drawdown does not capture how long you had to wait to recover. A high Sharpe ratio does not capture whether you will actually stay invested when prices fall by half.

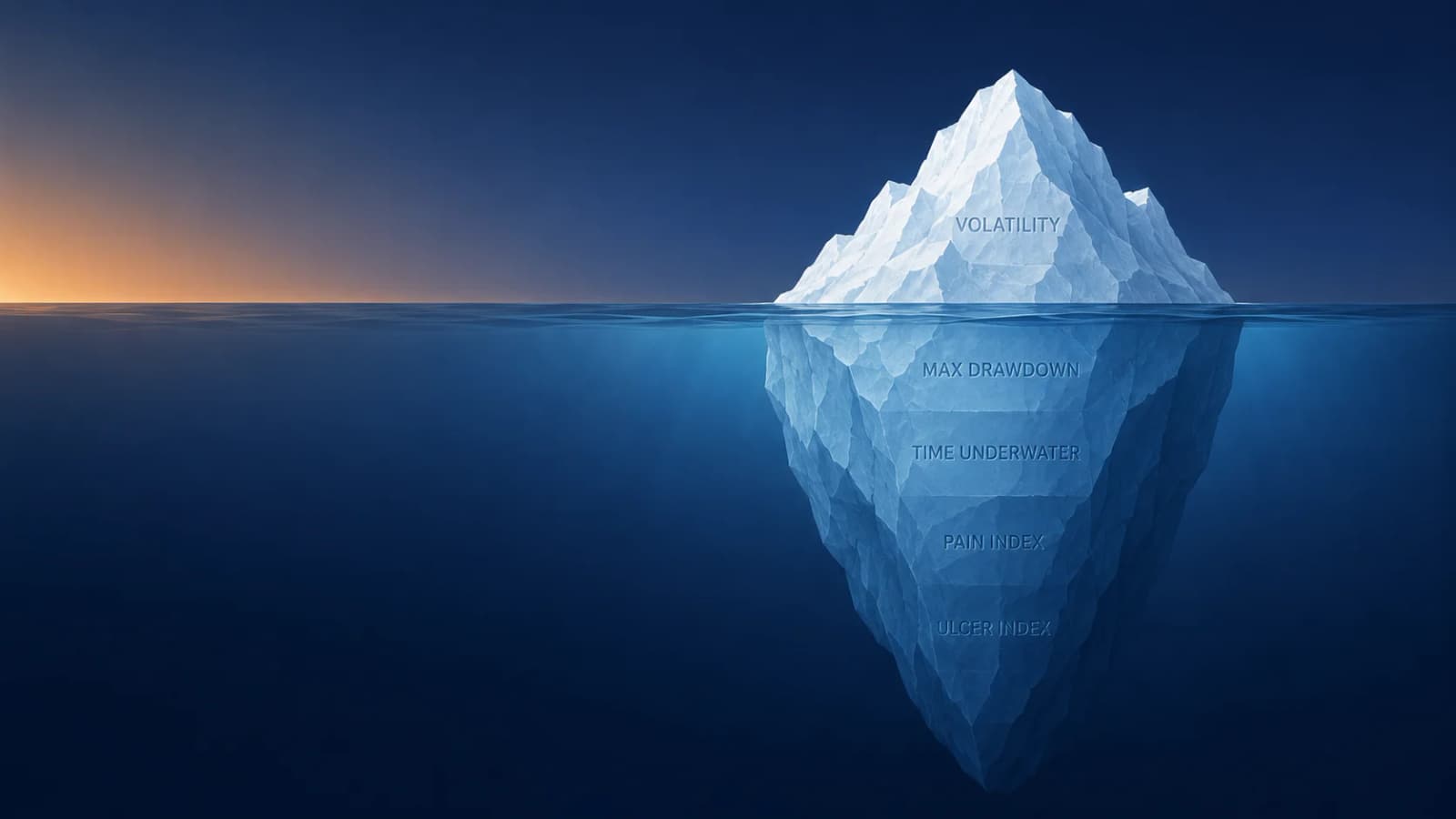

Summitward's position is that a useful risk dashboard has at least six numbers, not one. Volatility tells you about return dispersion. Maximum drawdown tells you about the worst single moment. Time underwater tells you how long the recovery took. Pain Index tells you about cumulative burden. Ulcer Index tells you whether the worst losses dominated. Sharpe and Sortino tell you about return per unit of risk, with caveats. Use them together. Each answers a different decision question.

Volatility: Useful but Incomplete

Volatility usually means the annualized standard deviation of returns. Fidelity describes standard deviation as a statistical measure of market volatility that rises when prices swing more widely around the average. Standard deviation is mathematically clean, comparable across portfolios, and central to most of modern portfolio theory.

The sample standard deviation of N periodic returns is:

where is the return in period and is the sample mean return. To annualize a monthly standard deviation, multiply by ; for daily data, use .

It also has a real problem: it treats upside and downside the same. A portfolio that jumps up 30% in a year contributes the same amount to standard deviation as one that falls 30%. Investors do not experience those moves the same way. The CFA Institute discussion of the Sortino ratio frames this directly: standard deviation penalizes large positive deviations the same way it penalizes large negative deviations, which is fine for engineering but often wrong for human decision-making.

Use volatility as a portfolio-engineering tool. Do not use it as the only definition of risk in a consumer-facing dashboard.

Maximum Drawdown: Intuitive but a Single Moment

Maximum drawdown is the worst peak-to-trough decline over a period. It is intuitive because investors understand the question: how bad did it get? Vanguard defines drawdown as the decline in value from a peak to a subsequent trough and notes that portfolios allowed to drift toward higher equity exposure can experience larger drawdowns. Vanguard's Principles for Investing Success makes the case for periodic rebalancing partly on those grounds.

Max drawdown has one structural advantage over standard deviation: it does not require any assumption about the distribution of returns. You just look at the worst observed decline. That makes it especially useful for strategies with fat tails (options-based income, leveraged ETFs, illiquid alternatives) where assuming normality understates true risk.

Max drawdown has a weakness too: it is a single number from a single moment in history. A portfolio that lost 50% in 2008 and recovered in 2009 has the same max drawdown as one that lost 50% and stayed flat for ten years. To an accumulator, those are different worlds. To a retiree drawing down monthly, they are nearly opposite.

Time Underwater: How Long Must You Wait?

Drawdown duration measures how long it takes to recover to the previous high. It is arguably more important for behavioral risk than the depth of the loss itself. A 25% decline that recovers in 8 months feels manageable. A 25% decline that takes 6 years to recover often breaks the plan, even though the trough is identical.

Two useful sub-metrics:

- Longest time underwater: the maximum number of consecutive months (or years, for annual data) the portfolio spent below its prior high. Captures the worst patience test in the sample.

- Current time underwater: if the portfolio is below its prior high right now, how long has it been? Useful for investors trying to decide whether they are in a normal pullback or a structural change.

Time underwater is where the Pain Index and Ulcer Index pick up, because both turn the underwater curve into a single comparable number.

Pain Index: The Area Under the Underwater Curve

The Zephyr Pain Index captures the depth, duration, and frequency of drawdowns in one number. Zephyr's own description frames the Pain Ratio as the analogue of the Sharpe Ratio, except the denominator is the Pain Index rather than standard deviation.

Mechanically, the Pain Index is the average drawdown over the measurement period, equivalent to the area between the 0% line and the drawdown curve divided by the time span. Using positive drawdown magnitudes:

A portfolio that spends most of its time at or near new highs has a low Pain Index. A portfolio that is frequently or persistently underwater has a high one, even if the worst single drawdown was not catastrophic. Swan Global Investments describes the Pain Index as measuring the "volume" between the break-even line and the drawdown line: deeper, longer, and more frequent losses all increase it.

Why this metric matters for DIY investors: it answers the question a max drawdown alone cannot. Two portfolios can share a 40% worst drawdown but spend wildly different amounts of cumulative time underwater. The one with the lower Pain Index spent more of its history compounding from new highs. That is the better lived experience even when the headline number is identical.

What counts as a normal Pain Index?

Computed from Damodaran's 1928–2025 annual return data, real (inflation-adjusted) Pain and Ulcer Index values for canonical portfolios fall in these ranges. Inflation-adjusted numbers are the honest comparison for long-horizon investors.

| Portfolio (real, 1928–2025) | CAGR | Max DD | Pain Index | Ulcer Index |

|---|---|---|---|---|

| 100% T-Bills (cash) | 0.3% | 45.8% | 20.4% | 25.8% |

| 100% US 10Y Treasury | 1.5% | 55.5% | 17.0% | 23.4% |

| Permanent Portfolio (25/25/25/25) | 3.5% | 25.9% | 3.4% | 7.1% |

| 60/40 (US Stocks + Bonds) | 5.1% | 35.2% | 6.4% | 11.2% |

| 80/20 | 6.1% | 42.6% | 8.8% | 14.4% |

| 100% US Stocks | 6.8% | 54.8% | 12.1% | 18.9% |

| 100% US Small Cap | 8.7% | 81.6% | 19.4% | 30.6% |

| 100% REITs | 1.1% | 34.6% | 6.5% | 10.1% |

| 100% Gold | 2.5% | 77.1% | 36.5% | 43.8% |

Three things worth noticing. 100% T-Bills shows a Pain Index of 20.4% in real terms, despite a 0% nominal Pain Index. Inflation is a silent drawdown, and this is the cleanest single illustration of why nominal-only risk metrics mislead long-horizon investors.

The Permanent Portfolio's 3.4% Pain Index is the lowest of any allocation in the table, even though its CAGR is below 100% stocks. That tradeoff is why drawdown-aware investors keep returning to it.

Gold's 36.5% Pain Index is the highest, driven by long real-return flat periods (the 1980s-1990s and 2012-2024) rather than single catastrophic crashes. Max drawdown alone would miss this.

Run the calculator below with the nominal toggle to see how dramatically these numbers compress when inflation is ignored.

Ulcer Index: Penalize Deeper Drawdowns

The Ulcer Index is a sibling metric that squares drawdowns before averaging them, then takes the square root:

Squaring punishes deep drawdowns more than shallow ones. A portfolio that spends two years 5% underwater scores lower than a portfolio that spends two years 30% underwater, even though both have similar Pain Index values. The Ulcer Performance Index uses Ulcer Index in the denominator as a Sharpe-style return-per-risk ratio. Portfolio Optimizer's explainer documents the formula and its applications.

When to favor which:

| Metric | Formula intuition | Best for |

|---|---|---|

| Pain Index | Average drawdown | Cumulative time spent underwater |

| Ulcer Index | Root mean square drawdown | Penalizing deep drawdowns more heavily |

| Max drawdown | Worst single drawdown | Worst-case historical gut check |

Risk-Adjusted Return Ratios

Sharpe, Sortino, Pain Ratio, and Ulcer Performance Index are all return-per-unit-of-risk ratios. They differ in the denominator:

| Ratio | Numerator | Denominator | Useful when |

|---|---|---|---|

| Sharpe | Excess return over the risk-free rate | Standard deviation | Comparing portfolios with similar return distributions |

| Sortino | Return above a minimum acceptable return | Downside deviation | Penalizing only the bad volatility |

| Pain Ratio | Excess return | Pain Index | Investors who care about time underwater |

| Ulcer Performance Index | Excess return | Ulcer Index | Investors most worried about deep drawdowns |

The Sharpe ratio divides excess return by total volatility:

where is the annualized portfolio return, is the risk-free rate, and is the portfolio standard deviation. Because counts upside and downside deviations equally, a portfolio that surges 30% is penalized the same as one that drops 30%.

The Sortino ratio swaps the denominator to fix that:

where is the minimum acceptable return and uses only returns that fall below it. The denominator swap is the entire difference: upside surprises no longer inflate the risk measure.

The Sortino ratio is worth pulling out because it directly fixes one of standard deviation's biggest weaknesses. The CFA Institute summary describes Sortino as excess return over the risk of not meeting an investor-specified minimum acceptable return, using only downside variation in the denominator. If you only care about falling short of a goal, that is closer to what you want than a symmetric volatility measure.

None of these ratios are magic. A portfolio with the best historical Pain Ratio is not guaranteed to be the best future portfolio. Use them to compare candidates, not to pick a winner outright.

One Number Cannot Define Risk, But One Can Summarize the Trade-Off

Investors often want a single number that answers whether a portfolio delivered enough reward for the pain required to hold it. The traditional answer is the Sharpe Ratio, which divides excess return by volatility. For long-term investors, an underwater period may be more meaningful than ordinary price movement.

Summitward uses the Martin Ratio (also called the Ulcer Performance Index) as its headline drawdown-adjusted return metric, branded for consumers as Underwater-Adjusted Return. It is the established Sharpe analogue that uses the Ulcer Index as its denominator:

where is the annualized portfolio return and is the matched-period risk-free rate (the T-Bill return measured over the same window). Higher values mean more annualized excess return per unit of deep-and-persistent drawdown risk.

Why not invent a Summitward Score that combines everything?

A weighted average of volatility, max drawdown, Pain Index, Ulcer Index, and recovery duration would look comprehensive, but it would double-count overlapping features of the same underwater path and embed subjective weights that have no objective justification. Bailey, Borwein, López de Prado, and Zhu showed that once a metric is used to rank historical strategies, it becomes easy to produce overfit winners whose apparent superiority does not persist out of sample. A custom composite score makes that trap worse, not better.

Why the Martin Ratio is the default here

The Pain Index is linear in drawdown depth. A 10%-underwater-for-12-months episode and a 20%-underwater-for-6-months episode have the same Pain Index contribution. They are not equally harmful in practice. Deeper drawdowns are more likely to trigger capitulation, forced selling, retirement-plan disruption, and behavioral mistakes. Because the Ulcer Index squares drawdowns before averaging, the Martin Ratio gives proportionally more weight to severe losses. That makes it the better default headline.

The Sharpe Ratio still matters

Martin Ratio complements Sharpe; it does not replace it. Sharpe remains the right comparison metric against industry research and portfolio-engineering frameworks. Martin is the right comparison metric when an investor is asking whether they got paid for the underwater periods they actually lived through. Show both.

Guardrails: the headline ratio is not a suitability test

A high Martin Ratio does not make a portfolio "best." A portfolio still has to clear independent hurdles:

- Maximum drawdown threshold: a single catastrophic decline can cause forced selling or abandonment regardless of ratio.

- Longest time underwater: a mathematically attractive portfolio can be emotionally unholdable.

- Real-return requirement: a very smooth portfolio can still fail long-term purchasing-power goals (see the T-Bills row above).

- Sequence-of-returns stress test: sequence risk near retirement is not summarized by any historical ratio. Run the Monte Carlo on the retirement dashboard for forward-looking checks.

- Concentration warning: employer stock or concentrated factor bets create risks not visible in any aggregate score.

- Short-history warning: attractive metrics from limited data can be misleading. Always look at the longest available track record.

One Slider, Three Metrics: The Drawdown Pain Spectrum

There is a simple way to see how Pain Index, Ulcer Index, and maximum drawdown relate. They are all the same family of metric with a different exponent p:

At , this is the Pain Index. At , it is the Ulcer Index. As , it converges on the maximum drawdown.

At p = 1, you average every drawdown observation equally. At p = 2, you square them first, so deep drawdowns count for more. As p grows, the formula converges on the single worst drawdown. The calculator below has a p slider so you can watch the ranking of two portfolios change as you move along this spectrum. That makes a useful point: which portfolio looks "safer" depends partly on how you weight depth versus frequency.

Risk for Accumulators vs Retirees

Drawdown metrics matter differently at different life stages.

For a 35-year-old saving regularly, a 50% bear market is mostly an opportunity. Contributions buy cheap shares. The portfolio recovers. The behavioral risk is real (panic selling locks in losses), but the financial risk is limited because future contributions and human capital dwarf the current portfolio.

For a 65-year-old drawing 4% annually, the same 50% bear market is an existential event. Withdrawals during a drawdown lock in losses permanently. Schwab's explainer on sequence risk describes the mechanic: the order and timing of poor returns can materially affect how long retirement savings last, even when the average return over the full retirement period is identical. For a deeper treatment of this, see the Summitward guide on sequence-of-returns risk.

This is why Pain Index, Ulcer Index, and time underwater become so much more important near and into retirement. A long flat or underwater period that is merely uncomfortable for a saver can force a retiree to sell at depressed prices, draining the portfolio faster than the long-run return assumptions suggested.

What Drawdown-Only Thinking Misses

Drawdown metrics are not the whole picture. Three risks sit outside them:

Inflation risk. FINRA notes that even conservative insured investments can carry inflation risk if they fail to keep pace with the cost of living. A cash-heavy portfolio can show nearly zero drawdown in nominal terms while quietly losing purchasing power for a decade. Always check real (inflation-adjusted) returns alongside nominal drawdowns.

Concentration risk. FINRA defines concentration risk as amplified loss risk from having a large portion of holdings in a particular investment, asset class, or market segment. Many tech-worker households look diversified at the account level (taxable, 401(k), HSA, Roth) but are economically concentrated in employer stock, human capital tied to one industry, local housing, and broad US growth-stock exposure. Drawdown metrics calculated on the index do not capture this. The Summitward guide on concentration risk covers the diagnostic framework.

Correlation under stress. Diversification is most valuable when it actually works during a crisis. Many asset pairs that look uncorrelated in calm markets become highly correlated in a sell-off. Backward-looking risk metrics computed over long periods smooth this out and can hide the regime-specific behavior. For deeper background, see Bernstein's four deep risks: inflation, deflation, confiscation, and devastation. Pain Index does not protect against any of those four.

The Summitward Risk Dashboard

Putting it together, here is the metric stack worth tracking for a DIY investor portfolio:

| Layer | Metric | Decision it helps you make |

|---|---|---|

| Return | Real CAGR | Is the portfolio actually growing purchasing power? |

| Variability | Annualized standard deviation | How wide is the return distribution? |

| Worst loss | Maximum drawdown | How bad was the worst historical decline? |

| Recovery | Longest time underwater | How long did the worst patience test last? |

| Cumulative burden | Pain Index | How much of history did I spend below previous highs? |

| Severe-loss weighting | Ulcer Index | Did the deepest drawdowns dominate the experience? |

| Risk-adjusted return | Sortino, Pain Ratio | Did I get paid for the downside I took? |

| Retirement specific | Bad early-return scenarios | Could a bad first decade force me to sell low? |

| Portfolio design | Concentration, correlation | Where is my real exposure? |

Read this as a decision dashboard, with each metric answering a different question. The right portfolio is the one you can hold long enough to capture its expected return, given everything the metric stack tells you about the path.

Portfolio Pain Profile Calculator

Most online risk-metric content explains formulas without ever letting you compare two portfolios and watch the differences. The calculator below uses Aswath Damodaran's annual return data (1928–2025) to let you set up Portfolio A and Portfolio B with any mix of US stocks, US bonds, T-bills, REITs, and gold. Move the p slider to see how the "safer" portfolio sometimes switches as you weight depth versus duration differently.

Reading the results honestly:

- Historical metrics describe what happened, not what will happen. A portfolio that backtested well over 1972–2025 may not repeat.

- Asset proxies are simplifications. Real REITs and gold portfolios have implementation costs, tracking error, and tax treatment that differ from the index series.

- The 1928 starting date includes the Great Depression, which is a tail event most portfolios will not see again. Move the start year forward to see how sample-period choice changes the ranking.

Who This Matters For

This framework helps different investors answer different questions:

- Accumulators with stable income: use it to set expectations before the next bear market. If you cannot stomach the historical Pain Index of a 100% stock portfolio, choose something you can hold instead.

- Near-retirees: use it to model whether your chosen allocation can absorb a bad first decade without forcing you to abandon the plan. Combine with Monte Carlo stress tests on the retirement dashboard and the safe withdrawal rate guide for the withdrawal side.

- Tech workers with RSUs: use it to remind yourself that the household-level Pain Index includes employer-stock exposure that the index-fund metrics ignore.

- Strategy shoppers: use it to pressure-test alternative ETFs and tactical funds. A clean Sharpe ratio over a short backtest does not guarantee a tolerable Pain Index over a full market cycle.

Who it does not help much:

- Anyone with money needed in the next one to three years. For short-horizon spending, the right answer is not "optimize Pain Ratio" but "do not expose this money to equity drawdowns at all."

- Highly active traders. Drawdown metrics on long-horizon buy-and-hold portfolios do not translate cleanly to frequently-rebalanced or leveraged strategies.

Final Takeaway

Use volatility, maximum drawdown, time underwater, Pain Index, Ulcer Index, and forward-looking stress tests together. Choose a portfolio you can hold through bad markets while still meeting your long-term goals. The single number worth less than any of these is whichever one you would have used to pick a portfolio by itself.

FAQ

Is the Pain Index better than maximum drawdown?

Different, not better. Max drawdown captures the worst single moment; Pain Index captures cumulative time underwater. Use both. Two portfolios with the same max drawdown can have very different Pain Index values, and that difference reflects a real difference in lived experience.

Why don't more professionals talk about Pain Index?

It is well-known inside institutional analytics platforms (Zephyr, StyleADVISOR, Portfolio Optimizer) but rarely surfaces in consumer-facing fund marketing because it makes most active products look worse than the marketing suggests. Standard deviation and Sharpe ratio are easier to anchor positive narratives to.

Does the Sharpe ratio capture downside risk?

Only indirectly. Sharpe uses standard deviation, which treats upside and downside the same. The Sortino ratio and Pain Ratio are better fits when the question is specifically about downside risk or time underwater.

Is volatility useless then?

No. It is the right tool for portfolio engineering (mean-variance optimization, risk-parity sizing) and for asset-pair comparison when distributions are reasonably symmetric. It is just an incomplete answer to "am I taking too much risk?"

How do I choose between Pain Index and Ulcer Index?

Pain Index if you care about how often and how long you are underwater. Ulcer Index if you care more about the depth of the worst losses. The drawdown pain slider in the calculator above shows you the smooth interpolation between them.

Do drawdown metrics apply to short-term goals?

Not usefully. For money needed in one to three years, the right framework is not optimizing risk-adjusted return; it is matching the asset to the liability. A high-yield savings account or short Treasury ladder has near-zero drawdown by design. Use Pain Index for portfolios you expect to hold across a full market cycle.

More in Investing & Portfolio

Browse all investing & portfolio guidesGet new guides by email

Evidence-based, no jargon. At most two emails a month. Unsubscribe any time.

Try it in Summitward

See portfolio factor analysis in action with your own financial data. Free to start, no credit card required.