Concentration Risk: When to Sell Your Company Stock and How to Diversify

Single-stock concentration increases volatility without increasing expected returns. Learn how to measure concentration with HHI, run the sell-vs-hold math, and use multi-year projections to build a diversification plan.

What Is Concentration Risk?

Concentration risk is the potential for outsized losses when a large share of your portfolio is tied to a single stock, sector, or asset class. For engineers and tech workers receiving RSUs, it shows up naturally: every vest adds more employer stock to a portfolio that is already correlated with the same company through salary, bonus, and future grants.

The danger is not just portfolio volatility. Your human capital, the present value of your future earnings, is already concentrated in your employer. If the company struggles, you face a pay cut or layoff at the same time your portfolio drops. Holding company stock creates a double exposure that diversified investors never face.

The quantitative framework for measuring concentration, the math behind the sell-vs-hold decision, and multi-year projections together build a diversification plan. For the tax mechanics of RSU vesting and the withholding gap, see the Equity Compensation guide.

Compensated vs. Uncompensated Risk

Not all risk earns a return. This distinction explains why concentration is costly.

Systematic (compensated) risk

Market risk, size, value, and momentum are systematic factors that affect broad groups of securities. You cannot diversify them away because they move the entire market. Investors who bear these risks earn a premium over time: the equity risk premium, the size premium, the value premium. This is the risk that drives expected returns.

Idiosyncratic (uncompensated) risk

Company-specific risk, such as earnings misses, lawsuits, management changes, or product failures, is idiosyncratic. Diversification eliminates this risk for free. A 500-stock index fund carries virtually zero idiosyncratic risk because the good surprises and bad surprises across hundreds of companies cancel each other out.

The punchline

Concentrating into a single stock increases your portfolio's volatility and skew (a fat left tail where a layoff and stock crash happen simultaneously) but does not increase expected returns. You are taking more risk for the same expected reward. The market does not pay you for bearing risk you could have diversified away.

A simple illustration: imagine two portfolios with the same expected annual return of 10%. Portfolio A holds one stock with 40% annual volatility. Portfolio B holds 500 stocks with 15% annual volatility. Over 10 years, Portfolio B delivers a tighter range of outcomes and a higher median terminal value (because volatility drag is lower), even though the arithmetic mean return is identical. Concentration destroys wealth in expectation through the mechanics of compounding.

Measuring Concentration: HHI

The Herfindahl-Hirschman Index (HHI) is a standard measure of concentration. It sums the squared portfolio weights of each holding:

HHI = w12 + w22 + ... + wn2

HHI ranges from near 0 (perfectly diversified across many holdings) to 1.0 (100% in one stock). In practice:

- Below 0.10: Well-diversified. No single position dominates.

- 0.10 to 0.25: Moderate concentration. One or two positions are large enough to matter.

- Above 0.25: High concentration. A single stock likely exceeds 40-50% of the portfolio.

The 10% single-position threshold is a common rule of thumb: if any one holding exceeds 10% of your portfolio, you are carrying meaningful idiosyncratic risk. For engineers whose human capital is already tied to that same company, even 10% may be too high.

Summitward's Concentration tab on the Portfolio page computes your HHI automatically from your holdings and flags positions above the threshold.

The Sell-vs-Hold Math

The sell-vs-hold decision turns on whether the stock's expected return is high enough to compensate for the uncompensated risk you carry by holding it.

Break-even return

When you sell company stock and buy a diversified fund, you pay taxes on any gain since the vest date. The break-even return is the annual outperformance the single stock must deliver to offset that tax drag and leave you at least as well off as the diversified alternative.

Consider a worked example. You hold $50,000 of company stock with a $40,000 cost basis (the vest price). If you sell, you owe long-term capital gains tax on the $10,000 gain. At a 15% federal rate plus 5% state rate, the tax is $2,000. You reinvest $48,000 into a total market fund.

If the diversified fund returns 10% annually, your $48,000 grows to $52,800 after one year. For holding the single stock to match that, it must return at least ($52,800 / $50,000) - 1 = 5.6%. That looks easy, but the stock must beat the market by 5.6% - 10% = -4.4%. Wait, that math suggests holding is better. Let us look more carefully.

The real question is not absolute return but risk-adjusted return. The single stock has roughly 2-3x the volatility of a diversified fund. Over longer horizons, the wider distribution of outcomes means the median outcome (what you actually experience) is lower than the mean outcome. A stock with 40% volatility and 10% expected return has a median 1-year return of about 2% (because of the volatility drag formula: median ≈ mean - 0.5 * volatility2). The diversified fund with 15% volatility and the same 10% expected return has a median of about 8.9%. The risk-adjusted math almost always favors diversification.

Summitward's sell-vs-hold break-even calculator on the Concentration tab runs this calculation with your actual cost basis, holding period, and tax rates, showing the exact annual outperformance hurdle your stock must clear.

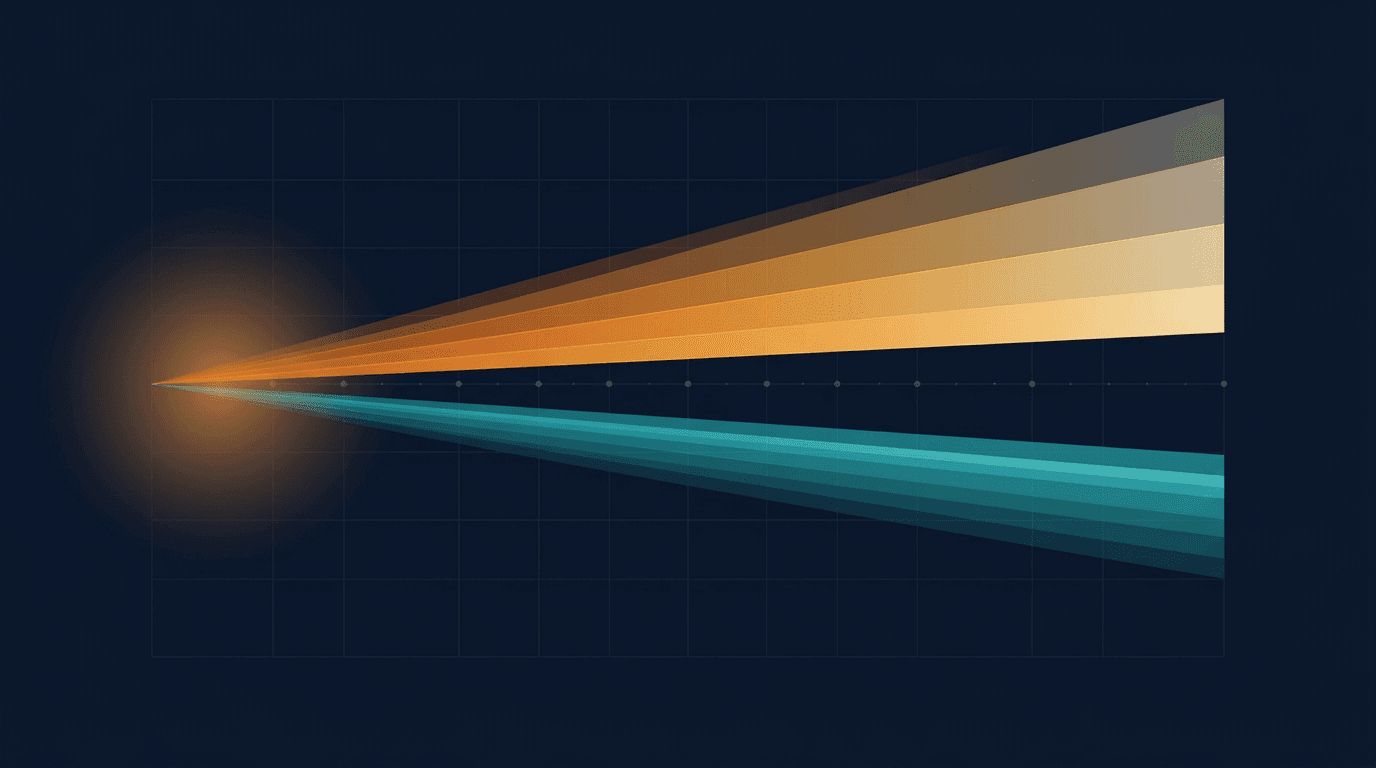

Multi-Year Projection: The Fan Chart

A single-year analysis misses the most important part: how outcomes diverge over time. Monte Carlo simulation projects thousands of possible paths for both the hold-concentrated and diversify-immediately strategies, showing the full distribution of outcomes at each future year.

The result is a fan chart with percentile bands (typically p10, p25, p50, p75, p90). Two things stand out when you compare hold vs. diversify:

- The hold path has wider bands. The p10 outcome (worst 10%) for a single stock is dramatically lower than for a diversified portfolio. This is the fat left tail in action: the concentrated portfolio has a meaningful probability of losing 50% or more over 5 years. A diversified portfolio almost never does.

- The medians converge or favor diversification. Because of volatility drag, the p50 (median) outcome for the concentrated portfolio is often lower than the diversified alternative, even when the expected (mean) returns are equal. Wider bands do not mean a higher center.

The visual makes the abstract concept of uncompensated risk concrete. You can see that holding a single stock gives you more ways to lose without giving you a higher expected payoff. Summitward's Multi-Year Diversification Projection generates this fan chart from your actual holdings, tax situation, and diversification timeline.

When Holding Makes Sense

The default should be to diversify, but there are legitimate exceptions. The key is to recognize these as reasons to accept temporary uncompensated risk, not reasons it does not exist.

- Tax efficiency on a small gain. If the stock has barely appreciated since vest and you are close to the long-term capital gains threshold (one year from vest date), waiting a few months to convert a short-term gain into a long-term gain can be worth it, as long as the position is a small percentage of your portfolio.

- Strong near-term conviction. If you have material non-public information (within legal trading windows) or a well-reasoned thesis on a specific catalyst, a short-term hold may be justified. But conviction should be time-bounded: set a date to re-evaluate, not an open-ended hold.

- Small position size. If employer stock is 2-3% of your total portfolio, the idiosyncratic risk is negligible. The transaction cost and tax hit of selling may exceed the diversification benefit. The 10% threshold is a reasonable trigger for action.

- Lockup or trading restrictions. Some companies impose blackout windows or post-IPO lockups. When you cannot sell, focus on diversifying everything else: direct new savings to diversified funds and avoid voluntary purchases of employer stock (ESPP proceeds excepted).

Common Mistakes

1. Anchoring on the grant price

RSUs are granted at a specific stock price, and engineers often anchor to this number. "The stock was $200 at grant and it is $150 now, so I should hold until it recovers." The grant price is irrelevant. Your cost basis is the vest price, and the sell-vs-hold decision depends on expected future returns, not past prices. The stock does not know what you paid for it.

2. Holding for LTCG when concentration is high

Waiting 12 months after vest to qualify for the long-term capital gains rate (15-20% vs. your marginal rate of 32-37%) makes sense in isolation. But if your employer stock is 30%+ of your portfolio, the concentration risk during that holding period can dwarf the tax savings. A 30% stock decline on a $200,000 position is a $60,000 loss. The LTCG tax savings on the same position might be $5,000-10,000. The expected value of the tax trade often does not justify the risk.

3. Confusing past returns with expected returns

"My company stock returned 40% last year, so holding it is better than an index fund." Past returns say nothing about future returns for a single stock. A diversified index earns a risk premium because market risk is compensated. A single stock's past outperformance is noise, not signal. Regression to the mean is the norm, not the exception.

4. Treating unvested RSUs as guaranteed

Unvested RSUs depend on continued employment. If you lose your job, you lose the unvested shares. Including them at full current value in your net worth overstates your financial position. A conservative approach: discount unvested RSUs by 30-50%, or exclude them from your FI number entirely and treat each vest as a bonus.

5. Gradual diversification without a schedule

"I will diversify over time" without a concrete plan usually means doing nothing. Set a specific schedule: sell a fixed dollar amount or percentage of your position each quarter, tied to vest dates if possible. Automate it if your brokerage supports it. A plan you execute beats a perfect plan you defer.

Action Plan

Here is a step-by-step process for managing concentration risk:

- Check your concentration. Look at your portfolio's HHI and the weight of your largest single position. If any stock exceeds 10% of your total portfolio, you have work to do. Use Summitward's Concentration tab for an instant read.

- Run the sell-vs-hold calculation. Enter your cost basis, holding period, and tax rates to see the annual outperformance hurdle. Ask yourself: do you genuinely believe the stock will beat a diversified index by that margin, adjusted for risk?

- Project forward. Use the multi-year diversification projection to visualize the range of outcomes for hold vs. diversify over 3-5 years. Pay attention to the p10 and p25 bands, not just the median.

- Set a diversification schedule. Decide on a target allocation (e.g., employer stock below 5% of portfolio) and a timeline to get there. Tie sells to vest dates to batch the administrative work.

- Coordinate with tax planning. Pair stock sales with tax-loss harvesting to offset gains. Consider spreading sales across tax years if the total gain is large. Use Summitward's Tax Projection page to model the bracket impact.

- Revisit quarterly. New vests add concentration back. Check your HHI after each vest and adjust your diversification plan accordingly.

Related Guides

Diversifying a concentrated position involves tax, portfolio, and planning considerations covered in these guides:

- Are We in an AI Bubble? Bernstein’s Four Signs is the behavioral companion: why concentration in a hot theme feels safe in a mania, and a stress test for surviving the drawdown.

- How to Sell Tax-Efficiently: SpecID and Tax Lots covers using lot selection to lower the tax cost of trimming a concentrated position.

- If Dimensional Gets Sold, Should Factor Investors Care? extends the sell-versus-hold tax break-even to bespoke factor ETFs and fund-sponsor risk, with a switching-cost calculator.

- You Have One Household Portfolio frames why concentration shows up at the household level across accounts, salary, and RSUs even when an individual account looks diversified. Includes a Household X-Ray calculator with asset-location flags.

- Modern Portfolio Theory for Real Life covers the marginal-fund test for evaluating diversification additions, with a portfolio-impact calculator using the two-asset variance formula.

- Sell Your RSUs at Vest is the entry-point post for the vesting decision: the cash-bonus test plus a side-by-side of sell-all, sell-to-cover, and deposit-cash. Pairs naturally with the break-even math in this guide.

- Most Stocks Lose to T-Bills gives the structural reason concentrated positions are uncompensated risk: only ~4% of stocks account for all market wealth, and you probably don’t hold one of them.

- The RSU Bridge Strategy makes the practical case for selling at vest by tying the proceeds to a household cash-flow system instead of letting employer stock compound.

- RSU Tax Strategy covers the tax mechanics of RSU vests and the sell-vs-hold framework for employer stock.

- Tax-Loss Harvesting shows how to offset capital gains from selling concentrated positions by harvesting losses elsewhere in your portfolio.

- Fama-French Factor Analysis reveals the hidden factor exposures a concentrated position introduces, and how diversification changes your risk profile.

- Lifecycle Asset Allocation explains how to set your overall stock/bond mix as you diversify from a concentrated position to a broad portfolio.

- Should You Buy IPO Stocks? covers the special case of IPO concentration, including the adverse-selection problem and the float-adjusted index mechanics for mega-IPOs.

- When to Sell a Winning Stock is the personal-anecdote companion to this guide: the behavioral, tax, and donation-of-appreciated-shares angles for an old low-basis YOLO winner, with a tax-cost-of-selling calculator.

Key Takeaways

- Concentration risk is uncompensated. Holding a single stock increases your volatility without increasing your expected return. The market does not pay you for risk you could diversify away.

- Human capital doubles the exposure. Your salary, bonus, and future RSU grants are already tied to your employer. Adding employer stock to your portfolio creates a correlated double bet.

- HHI above 0.10 is a warning. Any single position above 10% of your portfolio warrants a deliberate sell-vs-hold analysis, not passive holding by default.

- The fan chart makes risk visible. Wider percentile bands on the concentrated path, without a higher median, show you exactly what uncompensated risk looks like in dollar terms.

- A schedule beats a strategy. Decide what to sell, when, and how much. Automate where possible. The best diversification plan is one you actually execute.

More in Investing & Portfolio

Browse all investing & portfolio guidesGet new guides by email

Evidence-based, no jargon. At most two emails a month. Unsubscribe any time.

Try it in Summitward

See portfolio factor analysis in action with your own financial data. Free to start, no credit card required.